A windfall shows up — a bonus, an inheritance, a matured GIC, or just cash that’s quietly piled up in the chequing account — and the internet immediately hands you a fight. Dump it all in at once (lump sum)? Or drip it in over several months to be safe (dollar-cost averaging, or DCA)?

People agonize over this. So we modelled it on a Canadian household’s plan — $100,000 to deploy, a roughly $746,000 portfolio, a 30-year horizon, ten thousand simulated futures, all in today’s dollars. The honest answer is going to be annoying, because the debate everyone loves to have barely matters. The decision that actually costs real money is the one nobody frames as a decision at all.

The famous debate, settled: it’s a coin flip

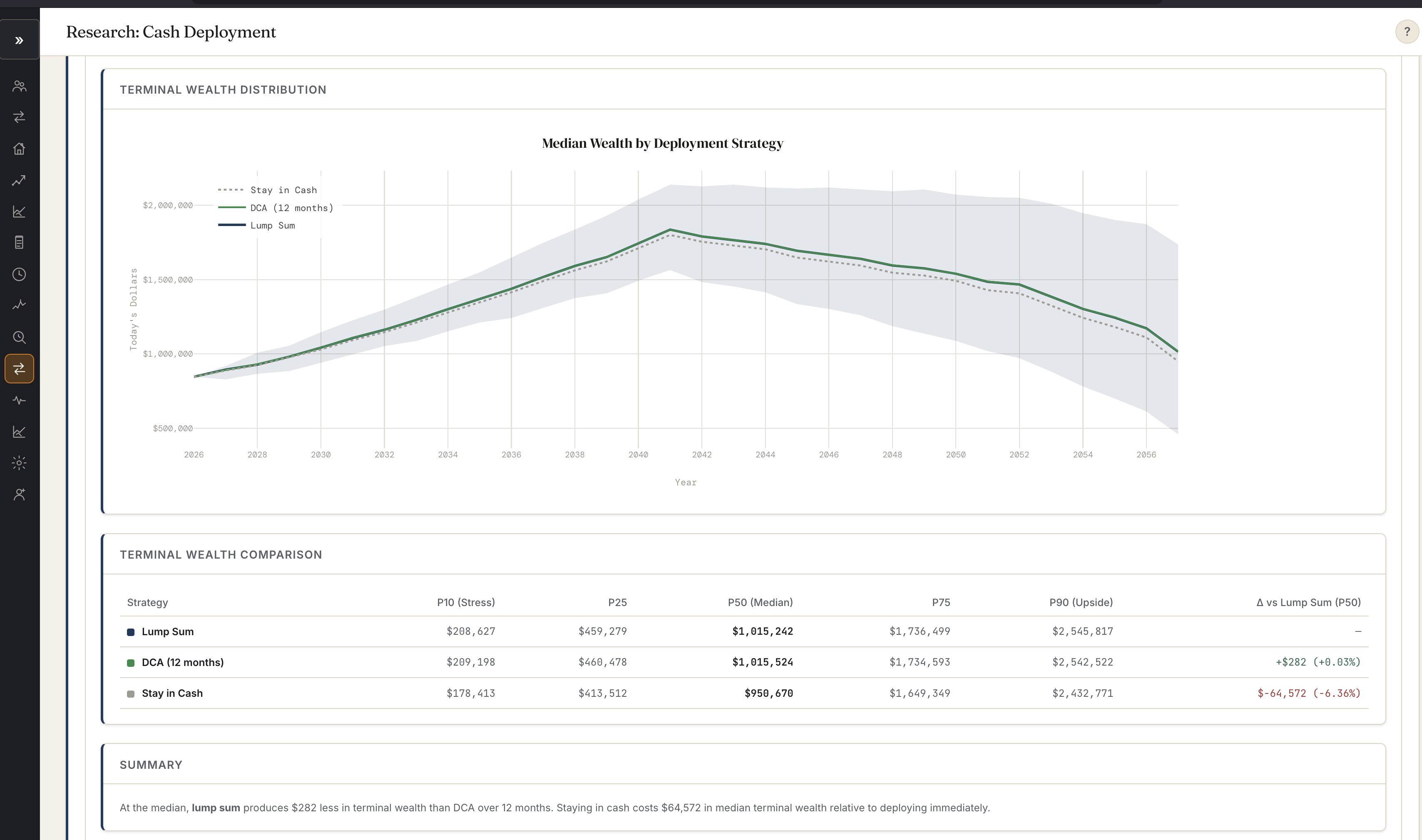

Here’s what deploying the $100,000 looked like at the median outcome:

- Lump sum (invest it all today): $1,015,242

- DCA (spread it evenly over 12 months): $1,015,524

That’s a difference of $282 on a million-dollar outcome. Call it 0.03%. And it’s not just the median: across the whole range, from the stressed 10th percentile to the optimistic 90th, the two strategies track almost exactly on top of each other. Lump sum edges some scenarios, DCA edges others, and the gap is always noise.

If you’ve ever lost an evening to this decision, here’s your refund: over a long horizon, whether you deploy a lump sum today or spread it over a year is, for practical purposes, a tie. The reason is simple — twelve months of drip-feeding is a rounding error against thirty years of compounding. The timing of the entry washes out.

The decision that actually costs you: staying in cash

Now the same $100,000, but you do the thing that feels safest — you wait. You leave it in cash “until things calm down.”

- Stay in cash: median $950,670

That’s $64,572 less than deploying it — a 6.36% haircut on the outcome, from one decision. And unlike the lump-sum-vs-DCA gap, this one doesn’t wash out in the noise. Cash loses in the good scenarios and the bad ones: even at the stressed 10th percentile, deploying the money left this household at $208,627 versus $178,413 for sitting in cash. There was no future in the simulation where waiting quietly won.

Why so brutal? Two reasons, and they compound. Cash isn’t in the market, so it isn’t participating in the growth that does the heavy lifting over decades. And in today’s-dollars terms — the only terms that matter — cash quietly loses to inflation while it waits. Every month it sits on the sidelines is time out of the market you never get back.

The uncomfortable takeaway: the “safe” move — parking it in cash until you feel ready — was the single most expensive choice on the table. The scary-sounding one — lump sum vs. DCA — didn’t matter.

So is dollar-cost averaging pointless?

No. But you have to be honest about what it’s actually for — because it’s not what people think.

DCA is not a return strategy. The returns are a wash; we just watched that happen. What DCA is, is a behaviour strategy, and it has two real jobs.

First, it gets you to actually invest. A plan you’ll follow beats a perfect plan you freeze on. If splitting the deposit into twelve pieces is the difference between deploying the money and leaving it in cash for two years “waiting for a dip,” then DCA just saved you that $64,572 — not through cleverness, but by getting you off the sidelines.

Second, it buys down regret. If you happen to deploy the whole sum the week before a bad stretch, spreading it in softens the sting of that specific unlucky timing. (Arthea has a “model initial drawdown” toggle precisely so you can see that scenario before it happens.) The median cost of that insurance is basically zero — which is exactly why “whatever makes you actually click deploy” is the right tiebreaker. Pick the one you’ll follow through on. That’s the whole decision.

The quieter question: where, not when

While everyone argues about when to deploy, the more valuable question is where. New cash is also your cheapest rebalancing tool — you can buy what you’re light on instead of selling something and triggering tax.

In this household, the target is 78% bonds, but drift had pushed it to 44% bonds and left it badly overweight US equity (40% against a 9% target). So the honest move for the $100,000 wasn’t “buy more of what’s been winning” — it was to steer the cash toward bonds, back in the direction of the plan. Deploy toward your target, not toward your favourite.

The point

The lump-sum-versus-DCA argument is the fun one to have on Reddit and the one that barely moves your outcome. The decision that genuinely compounds — for better or for worse — is how long the money sits doing nothing before it’s put to work. Stop optimizing the rounding error. Deploy the plan.

We’d rather show you the whole distribution and tell you plainly that the $282 is noise than sell you a clever-sounding timing strategy. The honest version of investing advice is often less exciting than the argument — and worth a lot more than $282.

See what deploying your own cash looks like — lump sum, DCA, or waiting — at arthea.ca.

Next in Field Notes: the tax move most Canadian DIYers miss — which account should hold which asset, and why it can quietly cost you more than your fund fees.

Arthea is an educational and analytical tool for Canadian households. The figures above come from one modelled household and depend on its allocation, horizon, and assumptions; your own numbers will differ. This is not investment, tax, or financial advice, and not a recommendation to buy or sell any security. Projections model uncertainty and are not guarantees of future results. Consult a licensed professional before acting.